- ESG ratings are widely used to assess the sustainability of investments

- “Sustainability” is a complex term and gets substituted by “environment” in our minds

- To align an investor’s wish for “sustainable investments”, ESG needs to be broken up:

- A clear focus on E only is imperative

The term “Sustainable Investing” is one among many other buzzwords used in the financial industry and it has increasingly gained popularity over the past years. Sustainable investing is oftentimes connected to the concept of “Green Investing” or ESG, which stands for Environment, Social, Governance.

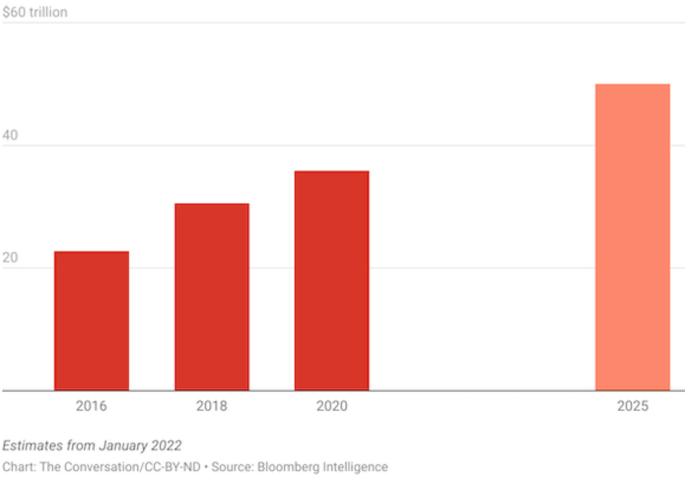

Currently, about one third of all investments under management use ESG criteria, while Bloomberg Intelligence projected that the total amount of these investments could reach $50 trillion by 2025. Asset managers can benefit from this trend by offering ESG funds to increase their total investments.

Figure 1: Projection of ESG investments in 2025.

Common shortcomings of ESG

Considering the magnitude of these investments, it is alarming that there still is no standard on reporting in place. This invites corporates and investment firms to use their own “ESG standards” which has led to countless greenwashing scandals. Additionally, major rating agencies are unable to construct coherent rankings. When MIT researchers analyzed the divergence of ESG ratings of six prominent ESG rating agencies in late 2022, they found that ratings could not even tell apart leaders from below average performers.

“In truth, sustainable investing boils down to little more than marketing hype, PR spin and disingenuous promises from the investment community.”

-Tariq Fancy, former Chief Investment Officer for Sustainable Investing at BlackRock

As a result, investors, be it retail, pension funds, or other institutions, whose goal is to invest sustainably, are left in the dark. Some might even go so far to argue that they are best advised to pick the stocks in their portfolio on their own.

The substitution process

So, ESG ratings are already questionable - but there is more. Not only cannot investors trust the ESG metrics and ratings put forward by all kinds of firms, but the concept of ESG ratings is problematic in itself. Let me explain this by taking a short excursion into behavioral psychology and heuristics, also understood as mental shortcuts.

The psychologist and Nobel Laureate Daniel Kahneman describes in his book “Thinking Fast and Slow” that if a satisfactory answer to a hard question is not found quickly, our brain’s automatic, fast-reacting response system will find a related question that is easier and will answer that instead. He refers to it as substitution process.

The target question is the assessment you intend to produce, while the heuristic question is the simpler question that you answer instead.

Here are two examples of the substitution principle:

When asked these questions, your feelings about financial crooks and the current standing of the president will readily come to mind. The heuristic question provides an easy answer to the more difficult question, while its meaning changes with it.

The substitution process in sustainable investing

This principle plays an important role in sustainable investing. In combination with the findings presented in the article “What Does Sustainability Mean? Perceptions of Future Professionals across Disciplines” (Damico et al., 2020) we understand why.

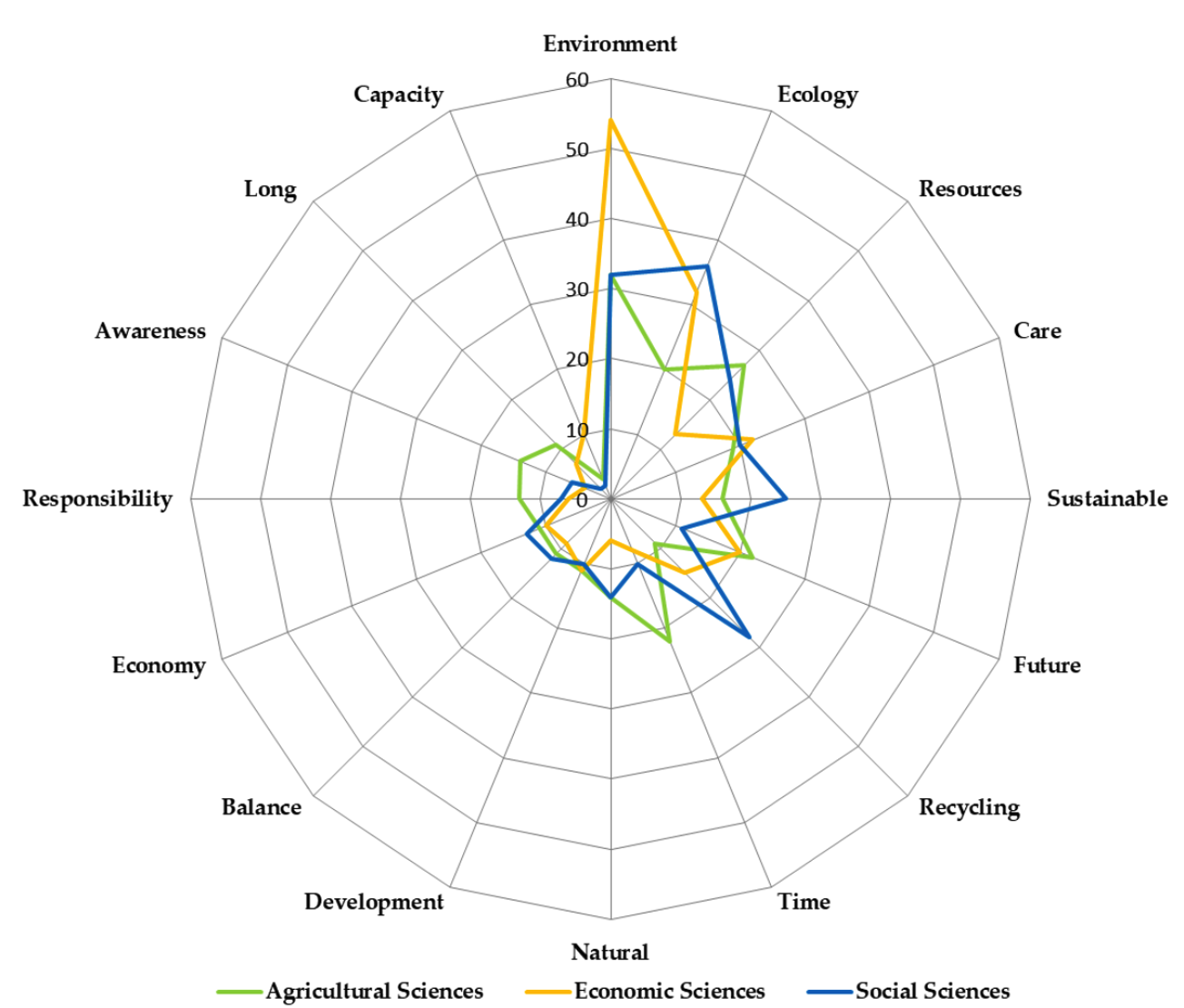

They analyzed what nearly 20,000 students of three different faculties of the National University of Lomas de Zamora, Buenos Aires perceived under the term sustainability. In line with studies of students and university leaders in China (n=1,134), the U.S. (n=1,389, n=82), and Germany (n=1,000), their results show that „in the minds of students, the concept of sustainability is highly linked to the environment”. To illustrate this, see figure 2 below, which pictures a comparison of words with 10 or more counts belonging to one of the themes in any of the faculties.

Figure 2: A comparison of words with 10 or more counts in any of the faculties.

With these discoveries in mind, the substitution principle can be applied to sustainable investing. If an investor’s goal is to construct a sustainable portfolio, chances are that they think of environmentally friendly companies instead. Social, not to speak governmental issues, only play a minor role. The following target and heuristic question illustrate this substitution process:

It will be found that most investors facing the target question, which includes the complex term sustainability, substitute it subconsciously into the simpler heuristic question which strongly focuses on the environment.

Here is an example from a real-world scenario:

In summer 2022, the electric-car manufacturer Tesla got kicked out of the S&P 500 index. The reasons for the removal were mostly related to governmental, and social issues, e.g. “codes of business conduct”, and only partly environmental.

This event led to newspaper headlines, many of which compared Tesla to the oil and gas-giant Exxon Mobile and sparked a debate about the integrity of ESG ratings.

Needless to say, when thinking of Exxon Mobile, the majority pictures one of the greatest environmental polluters out there. Tesla on the other side is viewed as quite the opposite.

This brief case study exemplifies that ESG ratings are not representing what investors, journalists, and the general public have in mind when thinking of sustainability. The comparison between Tesla and Exxon Mobil provides real evidence that their focus largely lies on E, while S and G are mostly disregarded.

Rethinking sustainable investing and ESG

These findings have further implications for the use of ESG ratings. Since most investors think of sustainability in terms of the environment, rating agencies should stop aggregating E, S, and G into a single measure.

A possible solution is to break up the rating into different topics, to implement clear, transparent standards, and make rating agencies, corporations, and investment firms liable when claiming that their fund is “green”.

Unfortunately, governments are slow to act or step in, and have a track record of lacking behind with policies regarding unprecedented developments in many domains, such as technology, but most importantly – climate change.

Therefore, it is time for the financial industry to wake up and face reality, which is: our time to curb a growing climate disaster is running down and we need an honest, effective effort to channel investments towards the right companies, now.