-

2022 was quite a turbulent year for financial markets worldwide

-

2023 started with a rally of equities and optimism among investors

-

We will take a look at whether the optimistic performance so far has a prerequisite to continue through the whole year.

Starting the story a bit earlier - in 2022, the global economy and stock market experienced a mix of ups and downs. The early part of the year was marked by optimism and steady growth, as various countries continued to recover from the impact of the COVID-19 pandemic. The rollout of vaccines and the easing of lockdowns fueled hopes of a return to pre-pandemic economic conditions. However, the inflationary pressures caused by supply chain disruptions and higher commodity prices put upward pressure on interest rates and caused investor concerns about the potential for higher inflation and interest rates in the future.

Macro outlook

As expected, many of last year’s troubles such as high inflation and commodity prices, world fragmentation, and the Russia-Ukraine conflict are here to stay in 2023 and will continue to cause investors headaches.

Figure 1: GDP Growth in 2023 (% change annualized)

Source: J. P. Morgan.

According to J. P. Morgan, Global GDP Growth is expected to be 1.6%, which is twice that of Developed Markets (0.8%) and way higher than the predicted growth of the Euro Area (0.2%). However, the Chinese economy is back on track after partially reopening its production facilities with a projected growth of 4% which, as expected, is much higher than the U.S. (1%).

Nevertheless, it seems that Jerome Powell’s soft landing is still on point, supported by a strong enough, for now, labor market and positive expectations of economic growth. On the other hand, analysts expect that Europe most probably will experience a mild recession. As a decisive factor is considered the high inflation already experienced and the decline in real income, consumption, and industrial production. According to Goldman Sachs, the real income of Europeans is expected to drop further until the end of Q2. Moreover, the fulfillment of gas storage facilities in Q4, and the price at which that will happen is also crucial for the inflationary pressure in Europe.

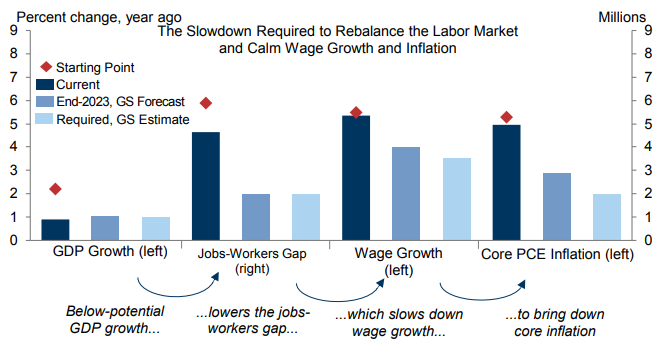

Figure 2: Goldman Sachs expects another year of below-potential GDP Growth in 2023 to rebalance the labor market and slow wage growth and inflation. However, CPI is still expected to be way above the target of 2%.

Source: Department of Commerce, Department of Labor, Goldman Sachs Global Investment Research.

According to Figure 2, the expected below-potential GDP Growth in 2023 will tighten the jobs-workers gap. Jobs-workers gap can be defined as a difference between the total number of jobs (employment plus jobs openings) and the number of workers. The tighter gap will slow wage growth and will decrease the pressure on core inflation because it will steer the labor market toward its equilibrium. Unfortunately, it will take much more time to get the inflation back to the 2% target, as reported by Goldman Sachs.

If inflation goes down, it means that the general price level of goods and services is increasing at a slower rate. This is often seen as a positive development for the economy, as it can result in lower costs for consumers, increased purchasing power, and a reason for the FED to pivot its contractionary monetary policy, boosting the prices of financial assets.

Asset classes expectations

The performance of different asset classes in 2023 will be influenced by a variety of factors, some of which were mentioned here so far. However, understanding the potential risks and rewards of different assets is an important part of constructing a well-diversified investment portfolio.

Figure 3: Different asset classes and their price expectations for 2023.

Source: Amundi.

Developed market equities

The bottom might materialize in mid-2023, making developed market equities’ valuations enticing. Analysts expect that non-US equity to outperform the US in the mid-run. Quality value stocks are on point, while defensive still expected to outperform growth ones given the unstable macroeconomic environment. However, high-quality cyclical is also worth considering. The main risks associated with developed markets are geopolitical friction and deeper- and longer-than-anticipated recession.

Developed market fixed income

Central banks will face increasing pressure on their credibility. Moreover, the trade-off between price stability and financial stability is also expected to rise. In Q1 and Q2 the short end of the US yield curve will be under pressure. In the Eurozone, credit spreads are expected to widen and default rates to increase reasonably, taking into account the indebtedness of some of the members.

Without considering any regional preferences, investment-grade bonds are preferred to high-yield ones. However, the US recession and deeper energy crises in Europe can be defined as potential risks.

Emerging Market Equities

Mainly positive equity returns are expected in 2023. During Q1 and Q2, preferred positions would be in Latin America and Emerging Asia, with a focus on Indonesia. Concerning the second half of the year, moving the valuation direction to countries from Europe, the Middle East and Africa, and Emerging Asia, which are involved in technological development such as Korea. The major risks related to EM Equities are policy mistakes, which could throw the countries into recession.

Bullish or bearish year - what to expect?

Despite the rally we saw in January, it is still early to come up with bullish conclusions. There are crucial market indicators that we need to pay attention to - CPI Index, GDP, and unemployment rate. The FED pursues the so-called “dual mandate” which means that it cares both about price stability and maximum employment. Hence, in case of favorable inflationary data and unemployment rise, the US Central Bank will pivot its hawkish direction and will boost the confidence of investors.

However, if this is not the case, the market can experience a downward trend, considering the fact the interest rates in the economy are at their highest point in the last 15 years. Companies should adapt to the environment of normal borrowing rates without continuous monetary stimulus.

So, it will certainly be an interesting year in which there will probably be no shortage of surprises and bullish and bearish sentiments will be fighting seriously over who gets to take over Wall Street.